Previous Story

AUD and NZD are ready to resume the fall

Reports about the possibility of postponing the signing of a trade agreement between the United States and China have contributed to the departure of markets in the lateral range. Volatility decreased, stock indices changed within 0.5%, with the exception of the Australian S & P / ASX 200 and New Zealand’s NZDOW, which grew by more than 1% at the end of the RBA meeting.

NZD/USD

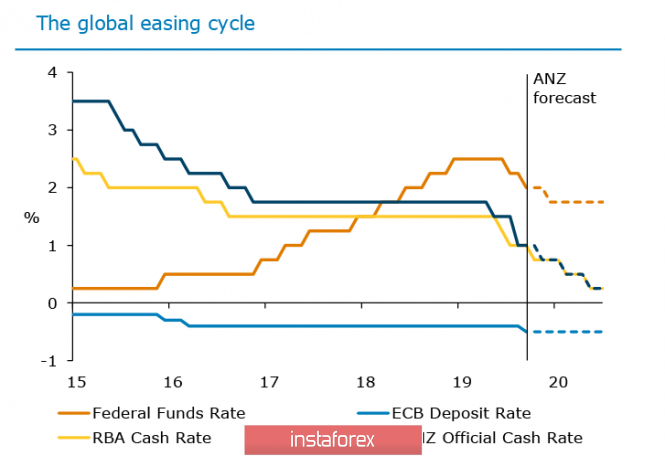

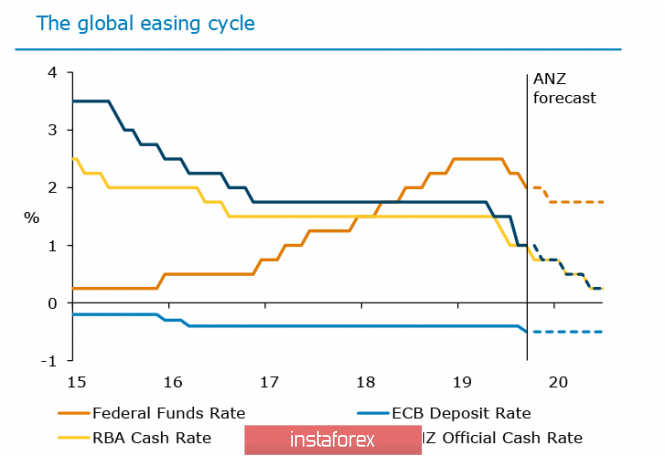

The outlook for New Zealand’s economy continues to deteriorate. RBNZ lowered its forecast of business optimism to -42.4 p, the lowest since March 2008, while ANZ notes a decrease in business activity deep in the negative territory to -3.5% in October against -1.8% a month earlier. On the other hand, unemployment resumed growth, in Q3 from 3.9% to 4.2%. Thus, the forecast for the RBNZ rate is deteriorating.

In addition, the RBNZ traditionally reduced the rate during periods of crisis, however, it was repeatedly emphasized in the last quarter that the reason for the reduction was not the crisis, but an attempt to stimulate spending and revitalize activity. There is no result, and RBNZ comments have already appeared on the possibility of using negative rates and other unconventional policy methods.

After the September meeting, the RBNZ issued an unexpectedly “hawkish” comment, but it had a very short impact on the markets. The expectations are that even a reduction in the Fed rate will not lead to a reduction in the spread of returns, since the RBNZ will reduce the rate even more aggressively.

The markets are forming a stable opinion that the RBNZ intends to hold another 3 rate cuts, the nearest of which will be in November, and by May 2020 – bring it to 0.25%. Accordingly, the yield on 10-year bonds tested below 1%. The slowdown in global economic growth will continue to put pressure on yields, so the spread between bonds of New Zealand and the USA will continue to increase, which also gives the direction of the movement of the NZD/USD.

Stable prices for raw materials somewhat compensate for this pressure, but the threat of a decline in kiwi is growing, which will be facilitated by the situation on global markets. The next RBNZ meeting will be held on November 13. On the other hand, the resistance zone 0.6330 / 50 has stood, and there is a high probability that the downward movement will continue. The immediate goal is 0.6331, the next is 0.6295 and further 0.6199. The prospect of moving to a psychological level of 0.6 i also growing.

AUD/USD

The Reserve Bank of Australia did not find any reason to reduce the rate at the meeting that ended on Tuesday, which was in line with market expectations and did not lead to an increase in Aussie. The expectation of the market include another rate cut in February, and the RBA is expected to consider not only a rate cut to 0.5% as a way to revive the economy, but also unconventional measures, such as an asset buyback program.

Since 2009 to 2016, leading Central Banks launched a total of 18 asset purchase programs, and only a third of them were directed only to government securities. The RBA may announce preparations for a similar program in February, along with a cut in rates. Therefore, markets will begin preparations for this large-scale event, which will put pressure on the Australian in the coming months.

Macroeconomic indicators still look weak. AiGroup Inflation Study indicates no positive change, Q3 inflation grew by only 0.5%, which corresponds to 1.7% y / y, while the price level remains below the RBA target.

Moreover, core inflation is 1.4% y / y, and is consistent with the overall weakness of the Australian economy. PMI in the services sector came close to the level of reduction, falling in October to 50.1p, while PMI in the construction sector declined to 43.9p., I.e. the sector has been declining for 12 months now.

The prospects for the yield spread between the bonds of Australia and the United States look the same as for New Zealand, and therefore, the pressure on the Aussie resumes. The upward trend, formed from the low of October 2, is coming to an end. Now, resistance zone 0.6323 / 29 corresponds to the upper boundary of the long-term channel, however, the chances of renewal are low. Thus, it is likely that the peak has already formed and the Aussie begins to fall in order to test a minimum of 0.6669. The nearest target is 0.6810 / 25, its fall can significantly accelerate the decline.

The material has been provided by InstaForex Company – www.instaforex.com