Previous Story

Your Comprehensive Guide to Creating Your Own Turtle Trading Strategy

Posted On 25 May 2014

Comment: 0

Turtle trading is the name given to a family of trend-following strategies. It’s based on simple mechanical rules to enter trades when prices break out of short-term channels. The goal is to ride long-term trends from the beginning.

Turtle trading was born from an experiment in the 1980s by two pioneering futures traders who were debating whether good traders were born with innate talent, or whether anyone could be trained to trade successfully. The turtles developed a simple, winning mechanical trading system that could be used by any disciplined trader, regardless of previous experience.

[adrotate banner= “65”]

The “turtle trading” name has been attributed to several possible origins. For me, it epitomizes the “slow but sure” results from this system. In contrast to complex black box systems, turtle trading rules are simple and easy enough for you to build your own system — I highly recommend it.

The earliest forms of turtle trading were manual. And, they required laborious calculations of moving averages and risk limits. Yet, today’s mechanical traders can use algorithms based on turtle parameters to guide them to successful trading. As always, the key to trading success lies in consistent discipline.

Which markets are best for turtle trading?

Your first decision is which markets to trade. Turtle trading is based on spotting and jumping aboard at the start of long-term trends in highly-liquid markets, usually futures. Since long-term trend changes are rare, you’ll need to choose liquid markets where you can find enough trading opportunities.

My favorites are on the CME: For Agriculturals, I like Corn, Soybeans, and Soft Red Winter Wheat. The best equities indexes are E-mini S&P 500, E-mini NASDAQ100, and the E-mini Dow. In the Energy group, I like E-mini Crude (CL), E-mini natgas and Heating Oil.

And, in Forex, it’s AUD/USD, CAD/USD, EUR/USD, GPB/USD, and JPY/USD. From the Interest Rate group of derivatives, I like Eurodollar, T-Bonds, and the 5-Year Treasury Note. Finally, in Metals the best candidates are always Gold, Silver and Copper.

Since turtle trading is a long-term undertaking with a limited number of successful entry signals, you should pick a fairly broad group of futures. Those above are my favorites, although others will work as well if they’re highly liquid. For example, in the past I’ve traded Euro-Stoxx 50 futures with excellent results.

Also, I only trade the nearest-month contracts, unless they’re within a few weeks of expiration. Above all, it’s critically important to be consistent. I always watch and trade the same futures.

Position size

With turtle trading, you’ll strike out many times for each home run you hit. That is, you’ll receive many signals to enter trades from which you’ll be quickly stopped out. However, on those few occasions when you’re right, you’ll be entering a winning trade at precisely the right moment – the beginning of a long-term change in trend.

So, for risk management your survival depends on choosing the right position size. You’ll need to program your mechanical trading system to make sure you don’t run out of money on stop-outs before hitting a home run.

Constant-percentage risk based on volatility

The key in turtle trading is to use a volatility-based risk position which remains constant. Program your position-size algorithm so that it will smooth out the dollar volatility by adjusting the size of your position according to the dollar value of each respective type of contract.

This works very well. The turtle trader enters positions which consist of either fewer, more-costly contracts, or else more, less-costly contracts, regardless of the underlying volatility in a particular market.

For example, when turtle trading a mini contract requiring, say, $3000 in margin, I buy/sell only one such contract, whereas when I enter a position with futures contracts requiring $1500 in margin, I buy/sell 2 contracts.

This method ensures that trades in different markets have similar chances for a particular dollar loss or gain. Even when the volatility in a given market is lower, through successful turtle trading in that market you’ll still win big because you’re holding more contracts of that less-volatile future.

How to calculate and capitalize on volatility – The concept of “N”

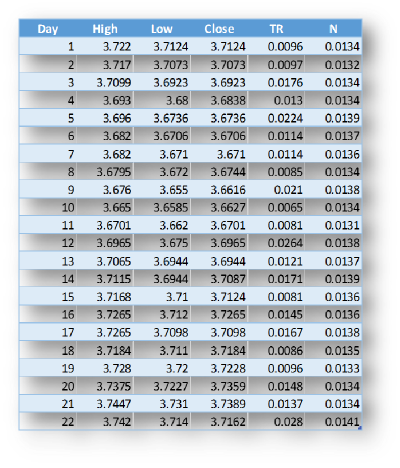

The early turtles used the letter N to designate a market’s underlying volatility. N is calculated as the exponential moving 20-day True Range (TR).

Described simply, N is the average single-day price movement in a particular market, including opening gaps. N is stated in the same units as the futures contract.

You should program your turtle trading system to calculate true range like this:

True Range = The greater of: Today’s high minus today’s low, or today’s high minus the previous day’s close, or the previous day’s close minus today’s low. In shorthand:

TR = (Maximum of) TH – TL; or TH – PDC; or PDC – TL

Daily N is calculated as: [(19 x PDN) + TR] / 20 (Where PDN is the previous day’s N and TR is the current day’s True Range.)

Since the formula needs a previous day’s value for N, you’ll start with the first calculation just being a simple 20-day average.

Limiting risk by adjusting for volatility

To determine the size of the position, program your turtle trading system to calculate the dollar volatility of the underlying market in terms of its N value. It’s easy:

Dollar volatility = [Dollars per point of contract value] x N

During times when I feel “normal” risk-aversion, I set 1 N as equal to 1% of my account equity. And, during times when I feel more risk-averse than normal, or when my account is more drawn-down than normal, I set 1 N as equal to 0.5% of my account equity.

The units for position size in a given market are calculated as follows:

1 unit = 1% of account equity / Market’s dollar volatility

Which is the same as:

1 unit = 1% of account equity / ([Dollars per point of contract value] x N)

Here’s an example for Heating Oil (HO):

For HO the dollars-per-point is $42,000 because the contract size is 42,000 gallons and the contract is quoted in dollars.

Assuming a turtle trading account size of $1 million, the unit size for the next trading day (Day 23 in the above series) as calculated using the value of N = .0141 for Day 22 is:

Unit size = [.001 x $1 million] / [.0141 x 42,000] = 16.80

Because partial contracts can’t be traded, in this example the position size is rounded downward to 16 contracts. You can program your algorithms to perform N-size and unit calculations weekly or even daily.

Position sizing helps you build positions with constant volatility risk across all the markets you trade. It’s important to turtle-trade using the largest account possible, even when you’re trading only minis.

You must ensure that the fractions of position size will allow you to trade at least one contract in each market. Small accounts will fall prey to granularity.

The beauty of turtle trading is that N serves to manage your position size as well as position risk and total portfolio risk.

The risk-management rules of turtle trading dictate that you must program your mechanical trading system to limit exposure in any single market to 4 units, your exposure in correlated markets to a total of 8 units, and your total “direction exposure” (i.e. long or short) in all markets to a maximum total of 12 units in each direction.

Entry timing when turtle trading

The N calculations above give you the appropriate position size. And, a mechanical turtle trading system will generate clear signals, so automated entries are easy.

You’ll enter your chosen markets when prices break out from Donchian channels. Breakouts are signaled when the price moves beyond the high or low of the previous 20-day period.

In spite of the round-the-clock availability of e-mini trading, I only enter during the daytime trading session. If there’s a price gap on open, I enter the trade if the price is moving in my target direction on open.

I enter the trade when the price moves one tick past the high or low of the previous 20 days.

However, here’s an important caveat: If the last breakout, whether long or short, would have resulted in a winning trade, I do not enter the current trade.

It doesn’t matter whether that last breakout wasn’t traded because it was skipped for any reason, or whether that last breakout was actually traded and was a loser.

And, if traded, I consider a breakout a loser if the price after the breakout subsequently moves 2N against me before a profitable exit at a minimum 10 days, as described below.

To repeat: I only enter trades after a previous losing breakout. As a fallback to avoid missing out on major market moves, I can the trade at the end of a 55-day “failsafe breakout” period.

By adhering to this caveat, you will greatly increase your chance of being in the market at the beginning of a long-term move. That’s because the previous direction of the move has been proven false by that (hypothetical) losing trade.

Some turtle traders use an alternative method which involves taking all breakout trades even if the previous breakout trade lost or would have lost. But, for turtle trading personal accounts I have found that my drawdowns are less when adhering to the rule of only trading if the previous breakout trade was or would have been a loser.

Order size

When I receive an entry signal from a breakout, my mechanical trading system automatically enters with an order size of 1 unit. The only exception is when, as mentioned above, I’m in a period of deeper-than-usual drawdown. In that case, I enter ½ unit size.

Next, if the price continues in the hoped-for direction, my system automatically adds to the position in increments of 1 unit at each additional ½ N price movement while the price continues in the desired direction.

The mechanical trading system keeps adding to my holding until the position limit is reached, say at 4N as discussed earlier. I prefer limit orders, although you can also program the system to favor market orders if you wish.

Here’s an example entry into Gold (GC) futures:

N = 12.50, and the long breakout is at $1310

I buy the first unit at 1310. I buy the second unit at the price [1310 + (½ x 12.50) = 1316.25] rounded to 1316.30.

Then, if the price move continues, I buy the third unit at [1316.30 + (½ x 12.50 = 1322.55] rounded to 1322.60.

Finally, if gold keeps advancing I buy the fourth, last unit at [1322.60 + (½ x 12.50) = 1328.85] rounded to 1328.90.

In this example the price progress continues in such a short time period that the N value hasn’t changed. In any event, it’s easy to program your mechanical trading system to keep track of everything on-the-fly, including changes in N, position sizes, and entry points.

Turtle trading stops

Turtle trading involves taking numerous small losses while waiting to catch the occasional long-term changes in trend which are big winners. Preserving equity is critically important.

My automatic turtle trading system helps my confidence and discipline by removing the emotional component of trading, so I’m automatically entered in the winners.

Stops are based on N values, and no single trade represents more than 2% risk to my account. The stops are set at 2N since each N of price movement equals 1% of my account equity.

So, for long positions I set the stop-loss at 2N below my actual entry point (order fill price), and for short positions the stop is at 2N above my entry point.

To balance the risk when I add additional units to a position which has been moving in the desired direction, I raise the stops for the previous entries by ½ N.

This usually means that I will place all my stops for the total position at 2 N from the unit which I added most recently. Yet, in case of gaps-on-open, or fast-moving markets, the stops will be different.

The advantages of using N-based stops are obvious – The stops are based on market volatility, which balances the risk across all my entry points.

Exiting a trade

Since turtle trading means I must suffer many small “strike-outs” to enjoy relatively few “home-runs,” I’m careful not to exit winning trades too early.

My mechanical trading system is programmed to exit at a 10-day low on my long entries, and at a 10-day high for short positions. If the 10-day threshold is breached, my system exits from the entire position.

The mechanical trading system helps overcome my greed and emotional tendency to close out a profitable trade too early. I exit using standard stop orders, and I don’t play any “wait and see” games…. I let my mechanical trading system make those decisions for me.

It can be gut-wrenching to watch my account fatten dramatically during a major market move with a winning trade, then give back significant “paper gains” before I’m stopped out. Still, my pet mechanical trading system works very well.

Turtle trading algorithms offer a quick way to build your own do-it-yourself mechanical trading system which is simple, easy-to-understand and effective.

If you have the discipline to keep your hands off and let your mechanical trading system do its job, turtle trading may be your best choice.

After all, turtles are slow, but they usually win the race……

Source: Comprehensive Guide to the Turtle Trading Strategy

What do you think about the Turtle trading strategy? Let us know in the comments below.

[adrotate banner= “70”]